Since the beginning of the century, pilots for weather index insurance (WII) for crops (Box 1), have been implemented in many developing countries – starting in Asia and South America before arriving in West Africa in the years 2010. In the Senegalese case, we are currently witnessing the multiplication of programmes that are either directly dedicated to WII or include a WII component as part of a larger rural intervention.

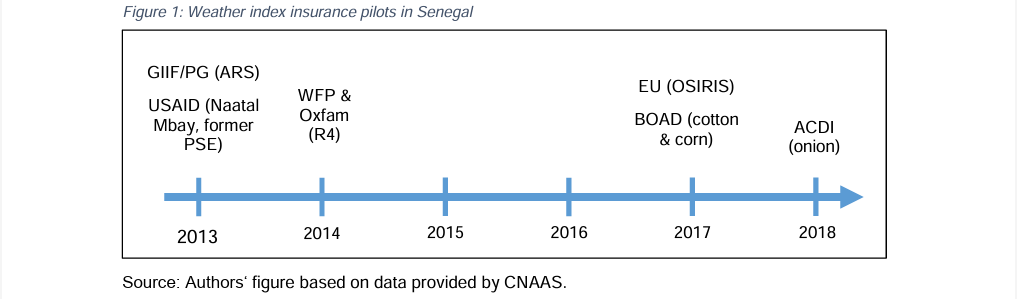

There are presently six projects that implement WII in specific areas of the country: Assurance Recolte Sahel (ARS) managed by Planete Guarantee (PG) and supported by the Global Index Insurance Facility (GIIF), Naatal Mbay funded by USAID, R4 managed by the World Food Programme (WFP) and Oxfam, OSIRIS funded by the European Union (EU), Index insurance for the cotton and the corn sector funded by the West African Development Bank (BOAD) and finally, index insurance for onion producers supported by ACDI (Figure 1). All these pilots provide WII through the only presently operating agricultural insurance company in the country, the Compagnie Nationale d’Assurance Agricole du Sénégal (CNAAS), which is a public private partnership created in 2008.

The intervention for which this evaluation is conducted is the WII component within the OSIRIS1 project. It is implemented through a savings and credit institution, COOPEC which is the financial branch of the farmers’ organisations network RESOPP. COOPEC and RESOPP as a union of 9 rural cooperatives are legally recognised and have been funded by the European Union to execute the OSIRIS together with their partners, including CNAAS. The overall purpose of the project is to strengthen economic and social inclusion of rural populations and to reduce vulnerability and chronic poverty in a context where small-scale agriculture is at the core of rural livelihoods.

OSIRIS aims to cover 12 500 farmers with agricultural insurance generally, of which 1500 are intended to be crop WII contracts. While the programme itself has started in January 2015, the WII component was delayed and started only in the rainy season of 2017. It is the first effective experience in Senegal of bundling WII with credit through using a micro finance institution as an intermediary. The product covers peanut harvests by transferring risks related to rainfall deficits to CNAAS. This aims to protect farmers by compensating them for rainfall-related harvest losses, to secure the loans which COOPEC/RESOPP provides to customers, and to stimulate investment in agricultural activities. Though these theoretical links are widely acknowledged, empirical evidence on impacts and the preferable way for bundling insurance with credit or other financial services is less conclusive (Zimmerman et al., 2016; Banerjee et al., 2014; Karlan et al., 2011; Gine and Yang, 2009).

| Index insurance definition Weather Index-based Insurance (WII) for crops is an insurance mechanism whose pay-outs are triggered by an index. This index is calibrated and triggered through rain gauge measurements on the ground. Next to WII, two other index insurance approaches are being used in different contexts: satellite-based indices, capturing remote sensing of vegetation levels, and yield indices, assessing historic trends and yield data. The weather-based index is used as a proxy for actual weatherrelated damage on the area covered by insurance. Given that the correlation between damage and rainfall is imperfect, basis risk, meaning the probability for the index to differ from actual events on a farmers’ field and therefore the potential to either falsely trigger or miss to trigger pay-outs, presents a continuous challenge for WII mechanisms. WII in Senegal In Senegal, only satellite and rain gauge based weather indices are developed so far. For the specific case of rainfall-based products, a rain gauge installed in a village chosen as a reference is used for the calibration of the index that triggers the pay-outs. A radius of 5 kilometres is covered by each rain semi-automatic or automatic gauge, which measures rainfall development. So far, all WII products offered in Senegal cover rainfall-deficits and delays, but not excess or other hazards. The produce covered so far are rain-fed rice, groundnut, millet, maize and cotton. Insurance provision channels have involved farmers’ organisations since the first pilots started in 2013 and microfinance institutions more recently. Both take on a role of aggregators and report the demand of their members or clients to a broker, Planet Guarantee (PG), who manages the design of the index and the delivery of the product on behalf of the only agricultural insurance company (CNAAS) in the country. A particularity of the Senegalese context is the fact that the government is a stakeholder in the public-private insurer and subsidises 50% of all WII premiums in order to support insurance development, which reflects an important commitment from the public sector. WII in this study The insurance product that is the object of this study is a crop WII product for groundnut, using an index based on rain gauge measurements on the ground. It is supplied by CNAAS through the broker PG, who is responsible for the design and the calibration of the index, as well as for the management of sales through the aggregator, in this case COOPEC/RESOPP, a microfinance institution linked to a country-wide network of farmers’ organisations. The produce covered by the WII product is two different types of groundnut: groundnut 90 days (90 days required for maturation) and groundnut 110 (110 days required for maturation). The average level of premium paid was 8524 FCFA (about 17$) and 11856 FCFA (about 21$) respectively. These premium values were derived from a premium rate ranging from 9.5% to 11.5% depending on the location of the rain gauge and the type of groundnut cultivated. The average surface covered was 1.4 hectares for groundnut 90 and 1.7 hectares for groundnut 110. For the payment options, farmers had the option to pay premiums in cash or to pre-finance them through credit, so that the total amount could be paid at the moment of loan reimbursement. In that case, the interest rate applied to the principal credit also applies to the insurance premium. |

This formative evaluation explores livelihood risks, along with farmers’ needs and preferences for financial mechanisms to manage these risks in the Senegalese peanut basin. Using a randomised controlled trial (RCT), we compare three sales protocols offered to three randomly composed groups of loan applicants to assess the effects of product bundling on WII take-up. Finally, we test assumptions and additional contributors and constraints to insurance take-up in Senegal through a mixed methods approach. The targeted knowledge gap this study addresses concerns the role that microfinance institutions have with regards to WII take-up in Senegal. While working with intermediaries, who can facilitate integration of different financial products and services, is one of CNAAS’s key strategies for boosting insurance demand, no independent studies have so far been conducted in the country to assess how much this approach potentially raises WII take-up and what effects it has on financial inclusion.